It’s now been six months since I realised I could realistically (semi-) retire by the time I’m 51, and ambitiously by 48. I’ve saved a bit of cash in that time, but TBH I’ve only just got into the swing of the early-retirement drive since the start of this year, 2015, so this isn’t so much of an update, rather a starting-point statement of where I’m at, a base from which to compare in the future.

I’ve now started (since January 3rd) to keep a record of everything I buy in various categories, with the intention that this will inspire me to spend less and save more. It worked a treat in January, but that’s probably because (a) it’s still a complete novelty and (b) I haven’t actually needed to buy anything of significant value.

At the moment my data’s only in Open Office, I might move it online laters.

January 2015 Early-Retirement Extreme Update

Reminder of Long Term Financial Goals –

- Be mortgage free in 7-10 years (£138k outstanding)

- Pay over £1000 a month towards the mortgage (15 year term) with a mind to either using savings or ‘trading down’ to pay off early.

- Save an absolute minimum of £250/ month in additional funds (=£30K after 10 years, without accumulations). Ideally this figure will be significantly higher.

- Find additional income streams to boost the above figure. Target = £20K in five years.

- Save £200 a month towards a ‘land fund’ – eventually to be used to purchase a van and land on which to establish a forest garden.

- Continue paying into the Teacher Pension Scheme.

January Update 1 – ‘Spending days compared to non-spending days’

I figure that I need to internalise not consuming – to this end I’ve started keeping a record of everything I buy and (roughly) how much it costs me. One of the interesting things that’s emerged is that there are several days during which I spend nothing and my non-spending days just over the 50% mark! This is now a new goal for 2015 – simply to clock up more non-spending than spending days.

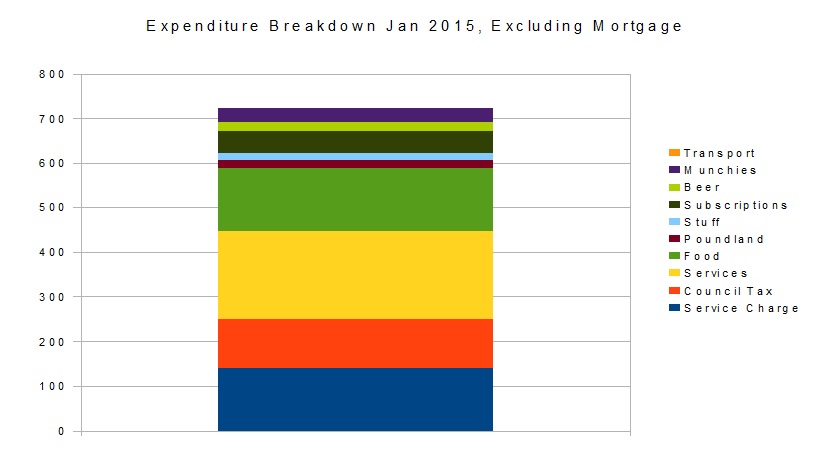

January Update 2 – Total expenditure excluding mortgage = £725 pounds

NB – Transport was £000.

January Update 3 – Expenditure including mortgage

- Frivolities = beer/ coffee/ subscriptions/ transport, (because I only really use transport for ents).

- Necessities = council tax, services, food, ‘stuff’ (because I’m not a frivolous materialist consumer).

- Property = mortgage repayments + service charge.

Ratio of expenditure to income including mortgage – 30%

Ratio of expenditure to income excluding mortgage – 71%

Summary

If I can keep this up for another 11 years, then I can basically move to full retirement – but this is premised on the following:

- Having a Teacher’s pension which kicks in at 60 (most of it anyway), meaning by the time I’m 51 (or thereabouts) I’ll have enough saved to simply see me through for 9 years.

- Continuing my very low consumption – After property my expenses come to around £600. I really don’t see why anyone needs to spend much more than this.

So – that’s me formerly started and outed on the ERE mission, bring it on!

Related Links

Early Retirement Strategies for the Average Income Earner (itunes)