It’s now been nine months since I realised I could realistically (semi-) retire by the time I’m 51, and ambitiously by 48. Here’s my four month in update

Reminder of Long Term Financial Goals – Update info in Italics

- Be mortgage free in 7-10 years (£138k outstanding)

- Pay over £1000 a month towards the mortgage (15 year term) with a mind to either using savings or ‘trading down’ to pay off early.

- Save an absolute minimum of £250/ month in additional funds (=£30K after 10 years, without accumulations). Ideally this figure will be significantly higher.

- Find additional income streams to boost the above figure. Target = £20K in five years. Only just starting – incidentally the reason I’ve stopped blogging here temporarily is because I’m trying to kick start some second income streams

- Save £200 a month towards a ‘land fund’ – eventually to be used to purchase a van and land on which to establish a forest garden.

- Continue paying into the Teacher Pension Scheme. NB – Neoliberal shaft 1 (although I new this was coming) – My pension is now effectively split – the bit I’ve got will be worth £7K a year at 60, everything I pay in from now won’t be worth touching until I’m 65.

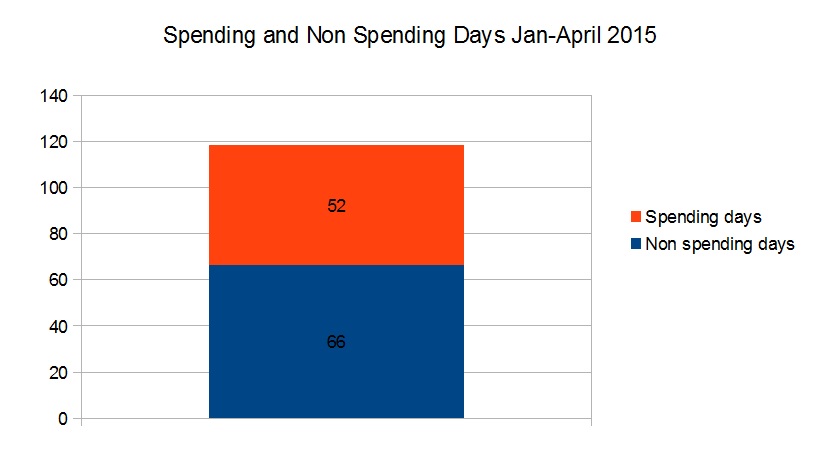

April update 1– ‘Spending days compared to non-spending days’

This is proving to be quite a successful strategy – It prevents me from buying the odd coffee when out or the odd munchie when at work, and makes me think more about buying things.

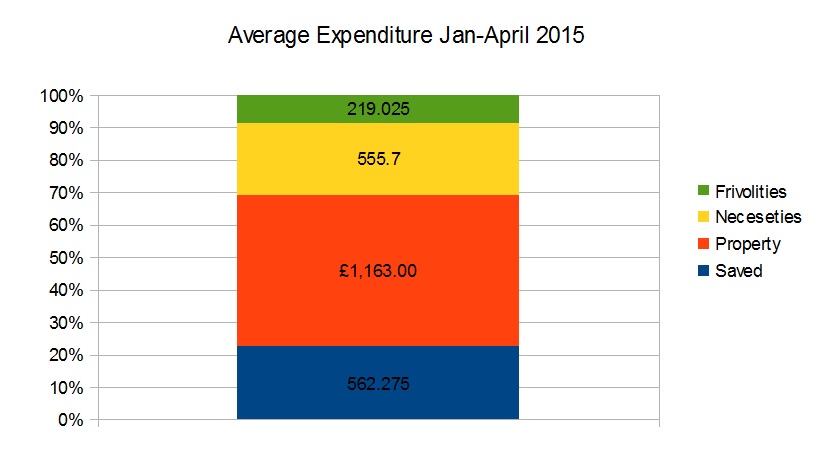

April update 2 – Summary of average monthly expenditure

- Frivolities = beer/ coffee/ subscriptions/ transport, (because I only really use transport for ents).

- Necessities = council tax, services, food, ‘stuff’ (because I’m not a frivolous materialist consumer).

- Property = mortgage repayments + service charge.

It’s not as good as the January update, but then again I guess the novelty has work off. This is a pretty realistic day to day expenditure tally, but it will get slightly worse once I start adding on occasional purchases such as computers and other gadgets which I only buy every few years at most.

Ratio of expenditure to income including mortgage – 30%

Ratio of expenditure to income excluding mortgage – 71%

In summary, after property, my expenditure is actually still only £750 a month. Given that the stress of work causes some of this, once work is ditched I could bring this down a little, say to £700, giving me an annual retirement expenditure of about £8500.

Not bad, I’ll give myself a B grade. Could do better.