January 2016 And I’m now one year in to my 7-10 year plan to (semi-) retire by the time I’m 51, and ambitiously by 48. This is the second of my intended 6 monthly updates, this allows enough time to show clear progress (hopefully rather than regress) and also these things to take quite a lot of time to review.

Executive Summary

-

Total Net Wealth gain of £27000 in 2015

-

Net wealth gain excluding equity – £9000

-

Average total monthly expenditure not including mortgage – £930

-

Average monthly savings of – £536

-

Average savings to expenditure ratio – 62% (if I include mortgage payments)

-

Overall I give myself 8/10 – For once I’m actually going to focus on the fact that I’m doing most things right, rather than the few things I could improve on.

Reminder of Original Long Term Financial Goals – Updates in Italics, YEARS COUNTED FROM JAN 2015.

-

Be mortgage free in 7-10 years (£133K outstanding)

-

Pay over £1000 a month towards the mortgage (15 year term) with a mind to either using savings or ‘trading down’ to pay off early.

I’m easily on track to do this in 10 years if I stay put in my flat in Surrey. However, the £140 I pay (in reality it’s probably more) towards service charge every month is becoming increasingly insulting, and so I’m looking at ‘downsizing’ to a house in a poorer area and commuting to work, POSSIBLY BY 2018.

-

Save £200 a month towards a ‘land fund’ – eventually to be used to purchase a van and land on which to establish a forest garden.

-

Save an absolute minimum of £250/ month in additional funds (=£30K after 10 years, without accumulations). Ideally this figure will be significantly higher.

In analytical terms I now treat these the same. I’ve done quite well here – my average overall savings each month is £537 – I made the decision in November to shove £140/ month into teacher’s AVCs, I’ve now decided to reverse that – I can’t access them until I’m 55 – what was I thinking?

NB The reason I keep banging on about land is because land squatting is a key part of my ERE strategy.

-

Find additional income streams to boost the above figure. Target = £20K in five years.

I’ve finally made some progress here – early days, more on this later as it develops.

-

Continue paying into the Teacher Pension Scheme.

It’s not quite a no-brainer to keep paying into this, but it still makes sense. The amount I pay in has increased, and because of recent changes to the scheme I’m now stuck with a pension at 60 of around £7K/ year – everything I pay in from now on is not worth claiming until I’m 65 – If I claim my future contributions at 60, I lose 25% of the value of current and future contributions (what I’ve already got is protected, but then again I’m sure this could change under the nasties.)

Now onto the more detailed updates…

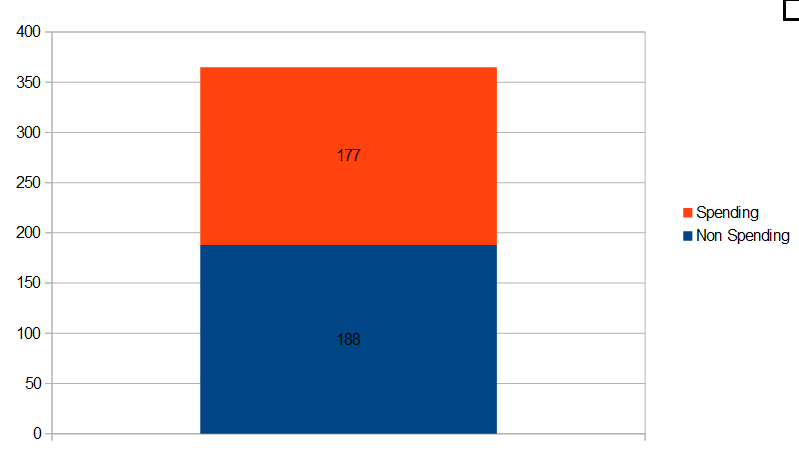

January 2016 Update One – Spending days compared to non-spending days

It was going so much better up until December – but still – I won by 11 days!

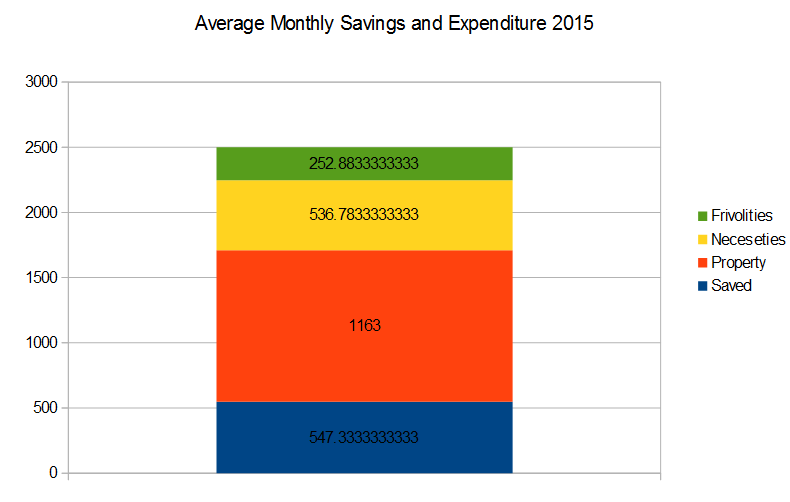

Jan-June 2015 Update Two – Expenditure and Savings Summary

-

Ratio of expenditure to income excluding mortgage –62% (down from 64% 6 month ave).

-

Ratio of expenditure to income including mortgage – 21% (down from 23% 6 month ave).

-

Frivolities = beer/ coffee/ subscriptions/ transport, (because I only really use transport for entertainment rather than work).

-

Necessities = council tax, services, food, ‘stuff’.

-

Property = mortgage repayments + service charge.

NB For calculating the above savings to expenditure ratio I always count service charge (an outrageous £140/month) as ‘expenditure’ but for the first calculation I count mortgage payments as savings because in the future my flat will act as an investment which will bring in an income (while I squat in a field).

Technically I should count the interest part of this as expenditure and the repayment as investment, but honestly I can’t be bothered to work this out and recalculate it every month as the repayments change, so stuff that! Just reduce the figure by a few percentage points if you’re uncomfortable with it.

January- June 2015 Update Three – Total average monthly expenditure excluding mortgage more detailed breakdown

This is really the headline figure – and it comes out at £930/ month, or £11K/ year – This is an honest account of how much I will need in retirement to live extremely comfortably. The service charge is something which is going to disappear hopefully very soon, but I figure the future cost of running a van which I currently don’t have will come out around the same amount of £140 a month, maybe more, so I’ll stick with £900 a month to live off. I’ve factored in £700 a month for my monthly retirement budget – this covers all of my necessities and allows £50 for ‘frivolities’ – so the idea is that Ill either need to suffer or do some kind of work to pay for me beers in retirement. Then again, that probably won’t be necessary as I’ll be enlightened by that point, and just naturally high on the joy of life.

Of course if I can pull off a land-squat my services costs will fall drastically, as will my food costs, so all of this could come down to nearer £5-600 in future. Whether that’s sustainable or not remains to be seen!

NB – The obvious immediate area for improvement besides service charge (PAIN!) is beer, I intend to hammer this down from September.

January Update 4 – Total Net Wealth

Well I’ve gained £27K TNW in the last year, but most of that’s equity, only £9K gained not including equity – still, that’s enough accumulated in one year to live for approx 1 year and 1 month.

I’ve basically got £32k to either go towards an early retirement fund or blow on some land to set up a land squat. Not bad for the end of year one!

It’s kind of comforting to know that that’s enough to buy some kind of Quinta in Portugal – I’ve even taken off £4K from the figure to factor in a contribution to selling up and moving on in case it comes to that! It also doesn’t include a small emergency fund I’ve got stashed away.

So all in all, I’m on track to achieve my ERE goals, I could do better, but I think this not so extreme route to retirement (land squatting aside) is sustainable!

If you like this sort of thing – then why not my book –

Early Retirement Strategies for the Average Income Earner, or A Critique of Curiously Ordinary Life of the Everyday Worker-Consumer

Available on iTunes, Kobo, and Barnes and Noble – Only £0.63 ($0.99)

Also available on Amazon, but for £1.99 because I’d get a much lower cut if I charged less!